How to Calculate Your True Home Buying Budget Beyond the Mortgage

How to Calculate Your True Home Buying Budget Beyond the Mortgage: A Guide to Hidden Expenses and Monthly Costs

Most people zero in on the mortgage payment when they start figuring out what they can afford — and that makes sense, because it's the biggest number on the page. But the mortgage is rarely the whole story. Property taxes, insurance, maintenance, closing costs, and a handful of other expenses quietly add up, and first-time buyers are often caught off guard by how fast they do. This guide cuts through the noise and walks you through every major cost — one-time and ongoing — so you can build a budget that reflects what homeownership actually costs, not just what the lender approves.

What Are the Hidden One-Time Costs When Buying a Home?

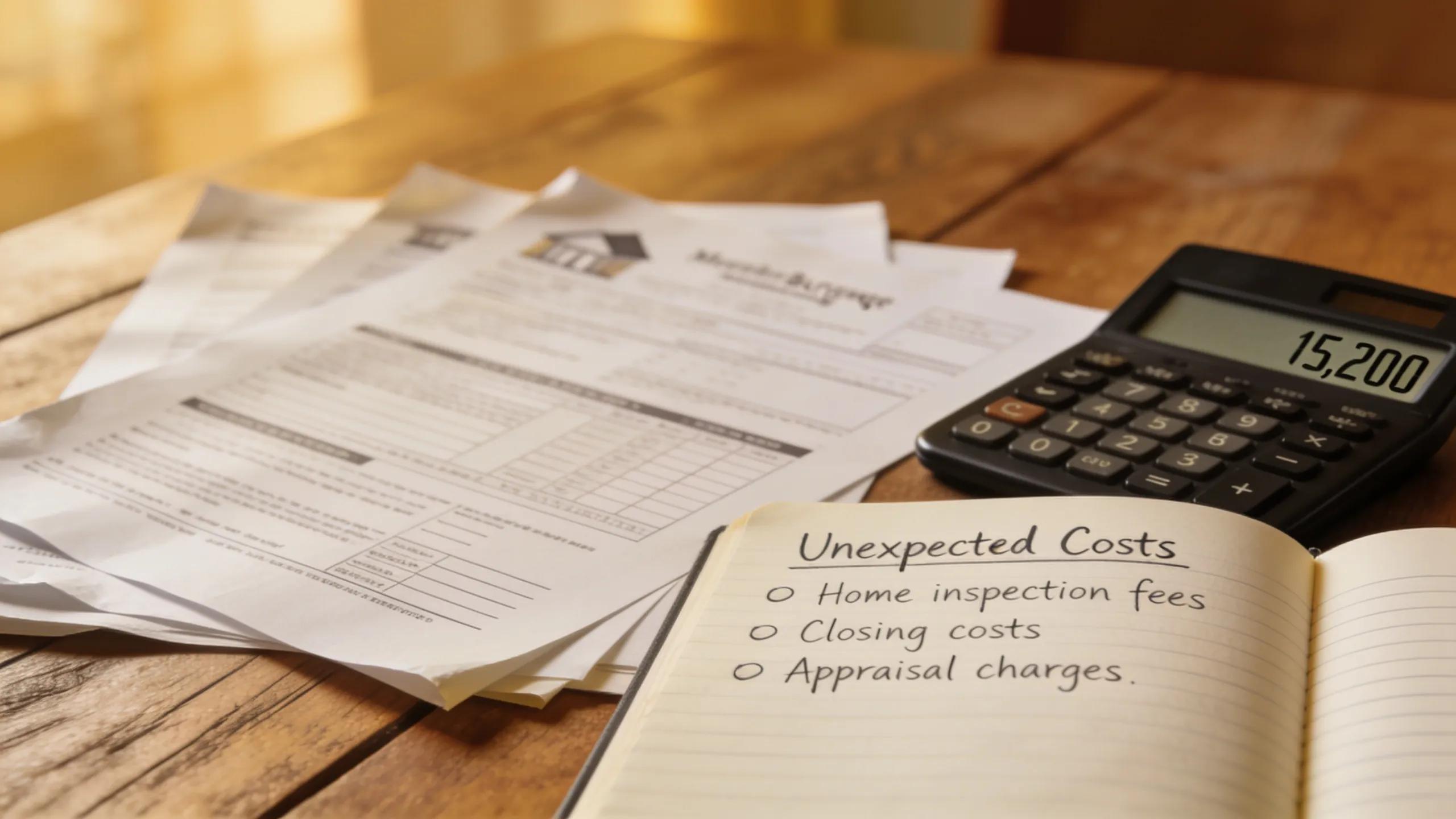

The sticker price on a home is just the starting point. Beyond the purchase price, a cluster of one-time costs tends to show up right around closing — and if you haven't budgeted for them, they can derail an otherwise smooth transaction. Knowing what to expect ahead of time puts you in control rather than scrambling at the last minute.

Which Additional Fees Should You Include in Your Purchase Budget?

Additional fees often overlooked in the home-buying process can include:

- Closing Costs: Typically ranging from 2% to 5% of the home's purchase price, these fees encompass various expenses like title insurance and attorney fees.

- Home Inspection Fees: Usually between $300 and $500, these fees are crucial for uncovering any potential issues with the property before purchase.

- Legal Fees: Hiring professionals to navigate the legal aspects of home buying can cost around $1,000 or more depending on your location and the complexity of the transaction.

Getting a handle on these fees before you sign anything keeps the process from becoming a financial fire drill at the closing table.

How Can You Accurately Estimate These Initial Home Buying Fees?

There's no single magic formula, but a few approaches together can get you pretty close:

- Online Calculators: Plug in your expected purchase price and most calculators will spit out a reasonable estimate of closing-related costs in seconds — a solid starting point.

- Real Estate Agents: A good agent has seen hundreds of transactions in your area and can tell you exactly what fees tend to pop up locally, saving you from generic national averages.

- Recent Sales Research: Look at what buyers in similar price ranges actually paid in your neighborhood. Real numbers from real deals beat guesswork every time.

Using a combination of these approaches gives you a far more grounded sense of what you're actually signing up for.

What Are the Recurring Monthly Homeownership Costs to Budget For?

Getting the keys is a milestone worth celebrating — but the financial picture doesn't freeze there. Once you're in, a steady stream of monthly costs takes the place of the one-time closing expenses, and these are the numbers you'll be living with for years. Mapping them out now means far fewer surprises down the road.

How Do Property Taxes and Home Insurance Impact Your Monthly Budget?

Property taxes and home insurance are two of the biggest recurring line items you'll face — and they're easy to underestimate if you only looked at the mortgage number:

- Average Property Taxes: Typically range from 1% to 2% of your home's assessed value, adding a recurring expense that must be factored into your budget.

- Home Insurance: The cost varies by location and home features, averaging about $1,500 annually, which translates to roughly $125 per month.

Both of these expenses tend to creep up over time, so it's worth building a little buffer into your monthly estimate from the start.

What Utility and Maintenance Expenses Should You Expect Regularly?

Beyond taxes and insurance, the day-to-day costs of running a home add up faster than most people expect. Here's what to plan for:

- Utility Bills: Gas, electricity, and water bills can vary widely; a typical household may spend around $200 to $500 monthly.

- Maintenance Scheduling Costs: Setting aside funds for regular upkeep is essential to preserve the home's value, generally recommended at about 1% of your home's value each year.

- Unexpected Repairs: Financial planners suggest keeping a repair fund of about 1-3% of the home's value yearly for unanticipated expenses.

Staying on top of regular maintenance isn't just good for the house — it's one of the smartest ways to keep unexpected repair bills from blindsiding your budget.

How Can Financial Planning Tools Help You Calculate Your True Home Buying Budget?

Spreadsheets and back-of-napkin math can only take you so far. The right financial planning tools do the heavy lifting — tracking what you expect to spend against what you actually spend, and flagging gaps before they become problems.

What Budgeting Calculators and Resources Are Available for Homebuyers?

There's no shortage of tools built specifically for homebuyers. A few worth having in your corner:

- Mortgage Calculators: Help you estimate monthly payments, including principal, interest, taxes, and insurance.

- Home Buying Expense Checklists: List potential one-time and recurring costs, ensuring you do not miss important budget allocations.

- Financial Planning Apps: Enable tireless tracking of monthly expenses against your budget, keeping spending in check.

Used together, these tools give you a real-time picture of your finances — not just a snapshot from the day you ran the numbers.

How Does Using Data-Driven Traffic Analytics Improve Home Buying Content?

Utilizing data-driven traffic analytics can significantly enhance home buying content delivery. Through tools that analyze consumer behavior and preferences, creators can tailor content to address common questions and pain points among homebuyers.

Advanced analytics allow for refining topics based on engagement, demonstrating a clear relationship between user needs and required financial education. By understanding what potential homeowners seek, more relevant and effective content can emerge. For example, understanding user search behavior can help optimize content using SEO analytics and keyword research.

Why Is Planning for Ongoing Maintenance and Unexpected Repairs Essential?

Ask any seasoned homeowner and they'll tell you the same thing: it's not if something breaks, it's when. The furnace, the roof, the water heater — these systems have a lifespan, and they don't check your bank account before they go. Planning for maintenance and repairs isn't pessimism; it's just smart ownership.

How Do Maintenance Costs Affect Your Annual Home Budget?

Maintenance costs can vary significantly; the typical household should budget 1% to 3% of the home's value annually for upkeep and repairs. Annualized costs should include:

- Routine Services: Such as HVAC servicing, plumbing inspections, and landscaping needs.

- Aging Home Considerations: Properties over 10 years old may require more frequent upgrades or repairs.

These aren't optional expenses — they're the cost of protecting what is likely your largest investment.

What Are the Best Practices to Prepare for Unplanned Home Repairs?

A little preparation goes a long way when something unexpected comes up. Here's how to stay ready:

- Creating a Repair Savings Fund: Aim for at least 1-3% of your home's value. This fund will help you manage unexpected expenses without disrupting your monthly budget.

- Regular Inspections: Schedule periodic checks on major systems like heating and plumbing to catch potential issues early.

- Seeking Professional Advice: Consulting with home maintenance experts can provide valuable insights into preventative measures that save money in the long run.

A dedicated repair fund means a broken water heater is an inconvenience, not a crisis — and that peace of mind is worth every dollar you set aside.

Categories

Recent Posts

GET MORE INFORMATION